If there’s one adult topic most people wish they’d learned earlier, it’s credit. It sounds simple until you try to rent an apartment, buy a car, or apply for your first loan — and suddenly, that mysterious number called a credit score decides how far you’ll go.

Building credit doesn’t have to be intimidating. In fact, once you understand the fundamentals, it’s just another life skill — like cooking, budgeting, or remembering to water your plants. The key is learning how the system works before it starts working against you.

So, let’s unpack what good credit really means, how to start from scratch, and what habits make the biggest difference.

Let’s be honest — most people only start caring about credit when they need it. You don’t think about it while you’re paying cash for coffee or splitting dinner with friends, but the moment you try to finance something big, credit becomes the gatekeeper.

So, what exactly is it?

At its core, credit basics come down to trust. When a lender gives you money — whether through a loan, a mortgage, or credit cards — they’re trusting you to pay it back. Your credit history shows how trustworthy you’ve been in the past. The better your record, the more opportunities you get in the future.

That trust is measured through your credit reports and ultimately reflected in your credit score. Think of it as your financial GPA. Every payment, every missed due date, every balance left unpaid — it all gets recorded. And lenders read that report before deciding whether to say “yes” or “no.”

It’s not about perfection. It’s about consistency and responsibility.

You might not need a credit card to survive day-to-day, but in the long run, credit shapes how easy (or expensive) life becomes.

Good credit helps you:

Bad or nonexistent credit, on the other hand, can make simple things harder. You might need a co-signer for a lease or end up paying higher deposits everywhere you go.

In short, credit doesn’t just affect your wallet. It affects your freedom.

Every adult who has ever borrowed money has a credit file. That file is maintained by credit bureaus — in the U.S., the main ones are Experian, Equifax, and TransUnion.

Your credit reports record all your financial behavior: open accounts, payment history, credit limits, balances, and even the number of times someone checks your credit.

Here’s the thing most people forget: credit reports aren’t just for banks. You can — and should — check them yourself regularly. It’s like looking in a mirror before a big meeting. You want to know if there’s spinach stuck in your teeth (or, in this case, an error lowering your score).

Federal law lets you access one free report from each bureau every year through AnnualCreditReport.com. Reviewing them doesn’t hurt your score. It’s the smart way to stay in control.

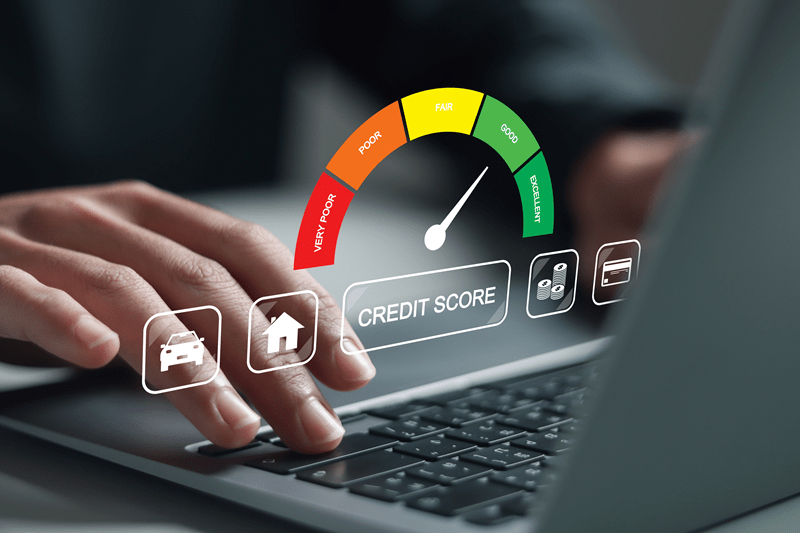

That little three-digit number follows you everywhere, but few people actually understand how it’s built.

Most scoring models (like FICO) use these key factors:

Together, these pieces tell your financial story. A late payment here, a maxed-out card there — they add up.

The magic number to aim for? A score above 700 is typically considered good, while 750+ opens doors to premium rates. But even if you’re starting below that, don’t panic. Scores can improve faster than you think when you practice responsible credit use.

Everyone starts somewhere. If you’re new to credit, the goal isn’t to rush — it’s to build a steady, reliable history.

Here’s how to start:

Get a secured credit card

This type of card requires a small deposit, usually equal to your credit limit. It’s designed for beginners and helps you prove you can handle payments.

Use it wisely

Don’t spend more than 30% of your limit. If you have a $300 card, keep your balance under $90. Paying in full each month is even better.

Make payments early

Late payments hurt your score the most. Set reminders or autopay to stay consistent.

Mix it up when you’re ready

Once you’ve built some history, you can add small loans or another card to improve your mix.

Patience pays here. Credit isn’t built overnight — but every smart choice moves you closer to a healthier profile.

Let’s clear up a myth: credit cards aren’t evil. They’re tools. How you use them determines whether they help or hurt you.

Used wisely, credit cards can build history, earn rewards, and offer protection against fraud. Used recklessly, they can trap you in debt before you even notice.

The trick is to treat them like debit cards — spend only what you can pay off in full. Don’t carry high balances or jump from card to card chasing offers.

Want a quick rule? If you have to think twice about affording it, don’t put it on credit.

Even the most responsible people slip up sometimes. These are the usual suspects:

Each mistake can shave points off your score — and it takes longer to rebuild than it did to damage it.

The best approach? Keep things simple. Fewer accounts, lower balances, consistent payments. That’s the formula that works every single time.

Here’s the good news — building solid credit doesn’t take forever. Most people can move from zero to “good” within six months to a year if they follow smart habits.

The not-so-good news? One late payment or default can undo months of progress. That’s why financial literacy matters just as much as discipline.

It’s not about memorizing credit jargon — it’s about understanding how your actions affect your score. That awareness makes all the difference.

If credit is power, responsibility is how you keep it.

Practicing responsible credit use means being mindful of your habits — not just paying on time, but knowing why it matters. It’s resisting the temptation to max out cards just because the limit allows it. It’s realizing that your credit score reflects more than numbers; it reflects behavior.

When you manage credit well, lenders trust you. That trust leads to better offers, lower rates, and more financial freedom.

Think of credit as a mirror — it doesn’t judge, it just reflects what you’ve done.

Maybe you’ve missed payments, or debt piled up during tough times. Don’t let that define you. Credit can be repaired — it just takes effort.

Start with these steps:

Rebuilding is slower than starting fresh, but it’s far from impossible. Lenders value persistence. As long as you keep showing progress, your score will recover.

Most schools never teach you about credit. That’s why so many adults feel lost when facing terms like APR, utilization ratio, or minimum payment.

Improving financial literacy doesn’t mean becoming an expert. It means asking questions, reading your statements, and knowing how to spot red flags.

It means learning that paying the minimum balance keeps you in debt longer, or that inquiries can slightly dip your score. The more you know, the more control you gain.

Knowledge turns anxiety into action — and that’s where confidence begins.

Here’s the thing: credit isn’t the destination. It’s the vehicle that gets you there.

You want to travel, buy a car, start a business, or own a home — all of that becomes easier when your credit works in your favor.

Strong credit gives you options. It turns “I wish I could” into “I can.”

So, while it might not be the most glamorous topic, understanding credit is one of the smartest investments you can make in yourself.

Building good credit is part strategy, part mindset. It’s not about chasing a perfect number — it’s about creating stability.

Start small, stay consistent, and check your progress often. Treat credit like a relationship: respect it, nurture it, and it will work for you, not against you.

And remember, mistakes don’t erase progress. They teach you. Every late payment, every lesson — it’s all part of learning how money moves.

Because once you understand the credit basics, you realize it’s not complicated after all. It’s just life, translated into numbers.

This content was created by AI